Have you heard about WISP Plus in the Philippines? You know what, it’s the latest SSS savings and investment program. Now, I bet you’re wondering how to invest in it, how it differs from the Pag-ibig MP2 or other investment stream, and how to pay and withdraw. For sure you’re doubtful if it’s a good and safe investment – I was too at first. That’s why it’s important to get to know the details. Well, you’re in the right place to get clarifications. I just attended a webinar about it and I’ll be sharing a complete guide on how to invest in WISP Plus SSS.

How to Invest in WISP Plus SSS: A Complete Guide

- What is WISP Plus?

- How to enroll in WISP Plus SSS?

- WISP Contribution Table

- WISP vs. WISP PLUS

- Pagibig MP2 vs. SSS WISP Plus

- How to Pay WISP Plus Online?

- How to Withdraw WISP Plus?

- Is WISP Plus a Good Investment?

- Is Wisp Plus a Safe Investment?

- What happens to my WISP Plus account when I die?

What is WISP Plus?

Last December 15, 2022, SSS launched a retirement savings program for its members in the Philippines.

- Workers’ Investment and Savings Program (WISP) Plus is an optional retirement savings program that is both an investment and a savings program.

- The WISP Plus serves as an additional layer of social security protection on top of the retirement benefits you will receive.

- It is an affordable, flexible, convenient, and tax-free savings plan.

- It caters to all members like you regardless of membership status, declared monthly earnings, and most recently posted monthly salary credit (MSC).

- Through your My.SSS account, you can join WISP Plus.

- For as low as P500, you can invest in WISP Plus.

- Continuous crediting of interest earnings after the 5-year maturity

- Has a 1% management fee to cover all expenses needed for operating the said fund

- Take note, you can only apply once in WISP Plus but membership has no expiration.

- According to SSS, for you to be eligible, you must not have applied for any final benefits claims, such as retirement or total disability benefits.

- Withdrawals can be made after the one-year holding period

- In case of extreme hardships or emergencies, you can withdraw it within one year

How to enroll in WISP Plus SSS?

For eligible members, WISP plus enrollment is through your account in the member portal. For registrants, it’s through the website upon approval of the SSS number application and will be automatically enrolled.

Let’s say you’re already an SSS member, here’s how you can enroll.

1. Sign in to your member account.

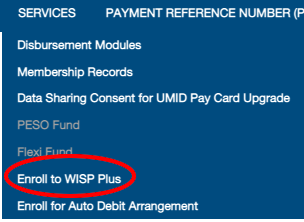

2. Click the “Services” tab.

3. Then, choose “Enroll to WISP Plus”.

4. View the terms and conditions. Once read, click “I Accept”.

And there it is1 Your WISP plus enrollment. Easy, quick, and hassle-free.

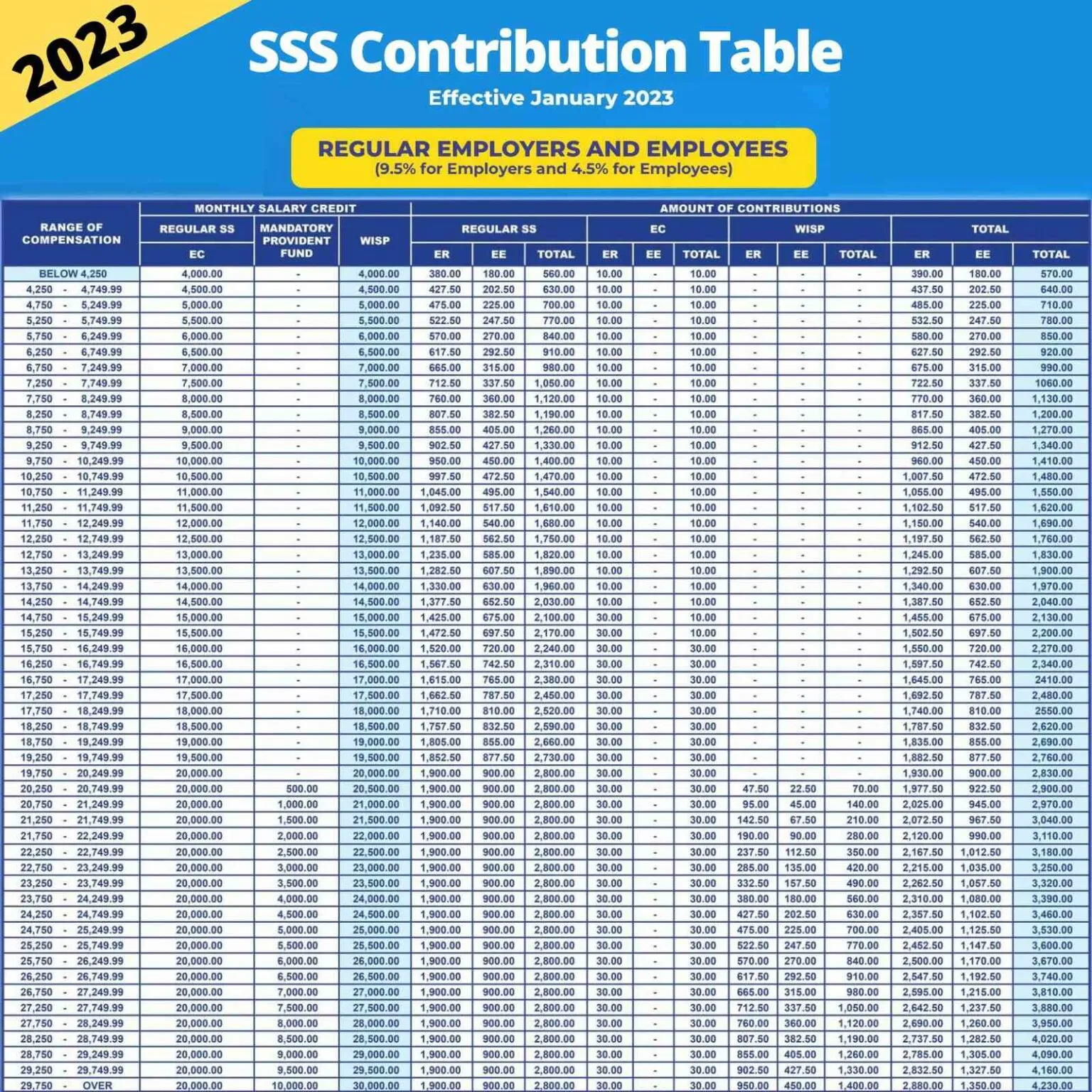

WISP Contribution Table

Before we dive into the difference between WISP and WISP Plus in the next section, take a look at the table below to see if your compensation has the corresponding WISP amount or if you exceed the monthly salary credit eligible for WISP. Who knows, through WISP you’ve already started investing and you just didn’t notice it.

WISP vs. WISP PLUS

According to SSS, WISP generates an income of P333.77 million and returns of 6.39% in its first year from the time it was launched in the Philippines. Its ROI surpasses the key market metrics like the 10-year Treasury bonds in the Philippines, which had a 2021 average yield of 4.1 percent.

But how does WISP differ from WISP Plus? Check this out.

- WISP is a mandatory provident fund (MPF) for members who have monthly salary credit (MSC) that exceeds P20,000 while WISP Plus is a voluntary investment program with no MSC requirement.

- Unlike WISP whose contribution amount is automatically computed based on what exceeds MSC, WISP Plus has a minimum contribution of P500.

- Because it’s part of your pension, your WISP earnings and principal are not withdrawable at any time. However, WISP Plus is withdrawable anytime as long as you’re already a member within 1 year under the emergency circumstance. If not due to emergencies, withdrawable after 1-year membership.

In addition, WISP and WISP Plus have separate tabs in your contributions as shown in the image below. You can check this too in your member account access.

Pagibig MP2 vs. SSS WISP Plus

And now you’ll ask what makes WISP Plus better than Pagibig MP2. Let’s know each feature as follows.

- You can invest a minimum of P500 for both Pagibig MP2 and WISP Plus which can be done not necessarily every month but anytime as long as you have extra money.

- Your funds (principal and profits) saved in WISP Plus won’t be “locked in” for five years unlike in Pagibig MP2 (though MP2 allows withdrawals under certain conditions for those less than five years). You can utilize WISP Plus for emergencies because it’s withdrawable at any moment (subject to terms and conditions).

- Pagibig MP2 and WISP Plus are both voluntary savings and investment programs.

- Both are applicable to members and are ideal for retirement purposes.

- Historically, Pagibig MP2 has a proven track record already and higher returns compared to WISP plus

- With WISP plus, you are limited to just one account, unlike in MP2 where it is allowed to have multiple accounts. Thus, you cannot play different strategies like the leveling MP2 Strategy we mentioned in this post: Pag-ibig MP2: 4 Tips to make the most out of Pag-ibig MP2

Thus, either of the two is worth considering an investment knowing that the contribution is affordable and flexible. You just need to check its features to know what’s best for you and fits to your investment goal.

How to Pay WISP Plus Online?

Once you’re enrolled in WISP Plus, you are ready to pay. So, how can you pay your contributions? You need first to generate the so-called Payment Reference Number (PRN) through your member account access. Then, you can pay at any sss branch, accredited banks, payment centers in the Philippines, or Gcash app using PRN.

Let’s first know how to generate the PRN of WISP Plus.

1. Generate Payment Reference Number (PRN).

a. Sign in to your member account and go to the “Payment Reference Number (PRN)” tab.

b. Click the “PRN > Contributions > Generate PRN” tab.

c. Fill in the necessary details as illustrated in the image below. Don’t forget to check “WISP Plus Only”.

d. Tap “Submit Request” and it will generate the PRN to be used in paying your WISP Plus.

Note: PRN is for sample purposes only.

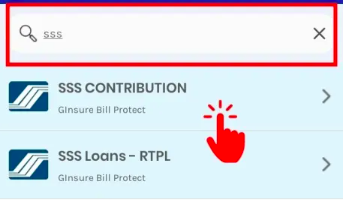

2. Paying WISP Plus through the Gcash app.

When using the Gcash app in paying your WISP Plus in the Philippines, make sure you already have your PRN with you. Then, follow the steps below.

a. Of course, you need to log in to your Gcash account.

b. Tap “Bills” and search for “SSS Contributions”.

c. Enter the needed information as shown below.

d. Cross-check the details and then confirm.

e. Once posted, you’ll receive an SMS or you can check it in your online record as well.

How to Pay WISP Plus Offline?

As mentioned earlier, paying WISP Plus SSS needs the generated PRN. So, you just need to print a copy of your PRN and bring it as you pay offline by visiting an SSS branch near you or any payment centers and accredited banks in the Philippines.

How to Withdraw WISP Plus?

As a WISP Plus member, you can withdraw the total accumulated account value (total contributions and investments) anytime under the following conditions:

- You must be a WISP Plus member for at least one (1) year.

- As mentioned previously, in case of extreme hardships or emergencies, you can withdraw it within one year

- You can withdraw a partial amount provided that the amount is based on the total accumulated account value posted prior to your withdrawal month, partial withdrawal applies once a month, and the remaining balance after withdrawal must not be lower than P500 pesos.

- You can withdraw the full amount within the first year of membership if you experience extreme hardship conditions like critical illness, involuntary separation from work, repatriation of an OFW member, and other conditions as determined by SSS.

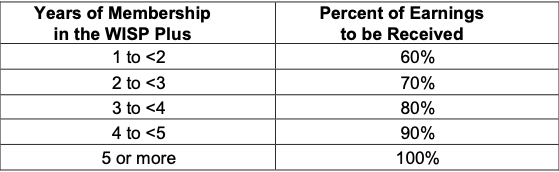

- You will receive adjusted earnings based on the below proportions.

Take note that when you withdraw the full amount of your total accumulated account value, you need to re-enroll to become a WISP Plus member again. Withdrawals are made through your approved disbursement account in your Disbursement Account Enrollment Module (DAEM) in SSS.

As mentioned earlier, your money is subject to a 1% management fee to cover all expenses needed for operating the said fund. This expense ratio can affect your compounding effect and affect the total proceeds you get. More guidelines, terms, and conditions of WISP Plus can be found here.

Is WISP Plus a Good Investment?

Now, you may ask if WISP Plus is really a good investment. So let’s have a scenario. Since your budget to contribute to this investment is only P500 pesos, so be it. Besides, it’s the minimum amount to invest as you learned earlier.

Let’s say you decide to contribute for 10 years as your retirement plan in the Philippines. So, P500 x 12 months in a year x 10 years is equal to P60,000, right? Then let’s say you reach 60 years old and you decide to use the invested money amounting to P1,500 per month for the next 10 years. By that time, you would receive P180,000.

You do the math. From the total amount of P60,000 contributions to P180,000 that you can possibly get – it may be good enough for your retirement years. It may be small for some of you but you see, a little amount per month for your golden years is better than nothing!

However, you’d say that you already have set aside for retirement years and probably would ask where else can you use the WISP Plus. Well, WISP Plus is also helpful for your kids’ educational fund, especially for newlyweds or new parents who are looking forward to long-term investments. Moreover, WISP Plus can be used for emergency purposes like critical illness that is under the terms and conditions mentioned above.

Related articles:

10 Best Online Investment Sites in the Philippines 2023

How to Invest in PERA (Personal Equity & Retirement Account)

Is Wisp Plus a Safe Investment?

Given that WISP Plus is government-backed by applicable laws and regulations like R.A. 11199 or the Social Security Act of 1997 in the Philippines, it’s guaranteed a safe investment. Accordingly, the investment will be spread across a variety of assets, including loans to pensioners (up to 70%), short- and medium-term loans to WISP Plus members (up to 25%), money market and BSP-approved investment instruments (up to 40%), and government securities (at least 15%), up to 20%, corporate and multilateral institutions, and equities.

Nevertheless, every investment has its risks. You might experience some of your investments having no ROI up until now or you already experienced loss. In fact, it is part of making investments. And as the popular quote says, “avoid putting all of your eggs in one basket.”

Related articles:

How to create an Investment Portfolio PART 1 ( Asset Allocation)

How to create an Investment Portfolio PART 2 ( DIVERSIFYING & REBALANCING)

What happens to my WISP Plus account when I die?

No doubt this question comes to your mind as I thought about it too. So in case death happens to a member like you, profits (anything claims determined by SSS in WISP Plus) will automatically go to your beneficiary/ies and will be disbursed to the beneficiary/ies’ approved disbursement account enrolled in SSS. Just a disclaimer, I haven’t found yet enough information regarding this on the SSS website. Thus, I’ll do more research and get back to you.

And that’s all about WISP Plus – making wise investments without taking on too much risk. This investment in the Philippines is a wonderful choice to start because of the guaranteed returns. If you’re trying to make an investment right now, WISP Plus SSS is unquestionably something to think about. Try to invest now!

Related Articles:

- 10 Appreciating Assets Every Woman Should Aspire To Own Philippines

- Best Investments in the Philippines UPDATED

- UPDATED: 12 Best Investments for Beginners in the Philippines

How to Invest in WISP Plus SSS: A Complete Guide

Hi Shei (sounds my nickname too hehe)…

To answer your question, every time you pay for wisp plus contribution you need to generate PRN because what amount appears on your generated PRN that’s what you need to pay for that particular month you decide to pay. Note that wisp plus is voluntary, thus, it’s not a monthly obligation that you need to pay.

In addition, wisp is the mandatory investment along with your regular contribution in SSS, provided monthly salary credit exceeds 20,000 which you can check on the SSS contribution table. Monthly PRN is a must here.

Hope I have answered your question:)

For more clarifications, feel free to reply here. Thank you!

Hi Ms. Sherie! May I ask if the PRN that generated is just once or do I need to generate PRN again if I have to contribute again on the following month?